The OCCC is required by law to track complaints and enforcement actions against Credit Access Businesses (CABs). Complaints against CABs are the lowest among all businesses regulated by the OCCC – one per every 21,000 transactions.

This is a manufactured crisis created by politicians, liberal activists, and the mainstream media intent on eliminating private sector credit options for underbanked Texans.

The reality is most private sector, short-term credit providers charge $15 to $20 per $100 borrowed. You would have to roll over and refinance your loan 26 times to reach an annual percentage rate of 400 percent. In reality, 71% of single payment loans are paid when due or refinanced once, while 92% of multiple payment loans are paid when due.

These are scare tactics designed to confuse the general public who have no need for these loans.

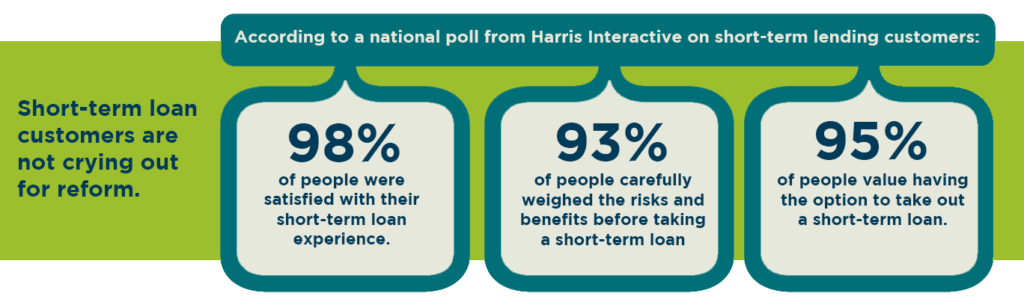

The OCCC requires that a CAB provide a disclosure before and after the loan that outlines repayment statistics, costs for other forms of credit, and the OCCC consumer complaint hotline. According to the OCCC, a majority of short-term lending customers pay their loans off as scheduled.

The OCCC tracks all short-term loans originated in Texas. According to the OCCC a majority of short-term lending customers pay off their loans as scheduled. It is a statistical outlier when a consumer rolls over their loans more than 6-7 times.

Public financial data shows the average Starbucks makes more than six times the profits of the average short-term lender. Wells Fargo, Citibank, Goldman Sachs, and PNC have net profit margins above 24%. Comparatively, the top three publicly traded short-term lending companies have single digit returns on investment.

According to the Federal Reserve Bank of New York, when Georgia and North Carolina banned short-term loans, households bounced more checks (over 1000 percent APR), complained more to the Federal Trade Commission about lenders and debt collectors, and filed for Chapter Seven bankruptcy protection at a much higher rate than those states without restrictions.1

After Austin and Dallas passed municipal ordinances, storefront lending decreased around 13%, but more expensive online short-term lending increased 19%. 2 According to the OCCC, municipal ordinances did nothing to reduce the demand or costs of credit throughout Texas.

1 “Payday Holiday: How Households Fare after Payday Credit Bans – February 2008 https://www.newyorkfed.org/research/staff_reports/sr309.html

2 Data provided by the Texas Office of Consumer Credit Commissioner

The community loan center program concentrated in South and East Texas has struggled to loan $38 million in five years.

The reality is socialist activists like Elizabeth Warren, Bernie Sanders, and Alexandria Ocasio-Cortez would prefer that the government provide tax payer subsidized short-term lending through the U.S. Postal Service rather than private sector credit options.

They are forced to comply with the Consumer Financial Protection Bureau’s 1,300 pages of regulations. In order to obtain a CAB license, they must comply with the Texas OCCC regulatory requirements. (http://occc.texas.gov/industry/cab)

Further caps, regulations, and burdensome requirements will force most short-term lenders to restrict credit access or simply shut down its operations.