An op-ed by Aaron Klein published at Brookings.edu

The explosion of overdraft fees makes basic banking expensive for people living paycheck to paycheck. Banks and credit unions generate over $34 billion in overdraft fees annually by one estimate. What those with money experience as ‘free checking’ is quite expensive for those without. Prior research has focused on who pays overdraft, finding a small number of people (9%) are heavy overdrafters accounting for 80 percent of the fees. Not as carefully researched is whether this is just a small part of banks’ general business model, or whether for some banks overdraft has become their main source of profit. In fact a few small banks have become overdraft giants relying on overdraft fees as their main source of profit. These banks are really check cashers with a charter. Why do bank regulators tolerate this?

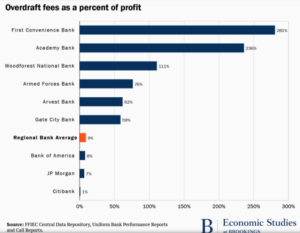

For six banks, overdraft revenues accounted for more than half their net income. Three had overdraft revenues greater than total net income (meaning they lost money on every other aspect of their business). First National Bank of Texas (doing business as First Convenience Bank) made over $100 million in overdraft fees yet posted an annual profit of just $36 million in 2020. Academy Bank and Woodforest National banks likewise made more money on overdraft revenues than profits in 2020. All three were entirely reliant on overdraft fees for any profit in 2019 as well. This is not a one-year blip; it is their business model. Armed Forces Bank, Arvest Bank, and Gate City Bank all rely on overdraft fees for more than half their profit.

Five of these six banks are national banks, regulated by the Office of the Comptroller of the Currency (OCC). Arvest Bank is a state-chartered institution whose primary federal regulator is the Federal Reserve (Saint Louis District), which seems to tolerate Arvest’s increasing reliance on overdraft as they went from 54 to 62 percent of total profit between 2019 and 2020. These regulators that allow banks to have a business model that depends on a single fee, charged only to consumers who run out of money, are not protecting the ‘safe, sound, and fair operation’ of the banking system.

It is disturbing that regulators tolerate banks that are mostly or entirely dependent on overdraft fees for profitability. Most of these are banks are regulated by the Office of the Comptroller of the Currency (OCC), but others are primarily federally regulated by the Federal Reserve and the FDIC has backup authority over all insured institutions. From a consumer protection stance, these entities operate more like check cashers and payday lenders than banks. From a safety and soundness proposition, reliance on this one highly costly fee is not sustainable. Don’t take my word for it: Oliver Wyman rang the alarm bell on overdrafts: “What should banks do about overdraft? We believe the crisis is accelerating the need to replace an antiquated product and an unsustainable value exchange.”

These are small banks, and most would be considered very small. Five had between $1 billion and $3 billion in assets (about one-hundredth the size of JPMorgan Chase). However, these banks may not even be the worst overdraft abusers. The smallest banks (those with assets totaling less than $1 billion) and most credit unions are not required to report their overdraft fee revenue at all. Researchers and consumer advocates have no idea how reliant they are on overdrafts. Unless bank regulators are asking these questions, the regulators may not know themselves. Regulators need to collect and publicize overdraft data for all banks and credit unions regardless of size.